Even after lawmakers pulled the plug on litigation incentives that Florida property insurers have long blamed for rising homeowner rates, there’s more insurance sticker shock ahead, experts say.

We can thank the increased frequency of catastrophic hurricanes and other costly weather events over the past few years, along with concerns that climate change will continue to send disasters our way, according to a recently released report.

The report was prepared by ALIRT Insurance Research, a Connecticut-based firm that analyzes the financial strength of insurers on behalf of insurance distributors, insurers, institutional buyers and analysts. Released on May 2, the report paints a dire picture of Florida’s insurance market and warns of a “no-win situation” for Florida-focused homeowner insurers monitored by the firm.

Reinsurance costs — which is coverage that insurers must buy to ensure they can cover claims after hurricanes and other catastrophes — could increase by up to 50% for Florida-based insurers before the June 1 start of hurricane season, the report said.

Such a steep increase could force insurers to pay more for reinsurance than they collect in premiums, which is “an unsustainable business model over the long haul,” the report said. Meanwhile, companies that cannot secure or afford desired levels of reinsurance could be left vulnerable to storm claims that could drive them into insolvency, according to the firm.

The pressures are evident in the shrinking pool of small domestic insurance companies that have formed to serve homeowners in the state since 1992’s Hurricane Andrew. A pool of companies monitored by ALIRT has shrunk from 42 companies in 2021 to 33 currently. Eight Florida-based companies have gone insolvent since 2021, the report notes.

The 33 surviving companies exclude subsidiaries of large companies like Allstate, Farmers, Progressive, State Farm, Travelers and USAA that were created to insulate the parent companies by focusing solely on Florida risks.

Thirty of the 33 surviving Florida-focused companies have financial strength scores well below the national average of companies that ALIRT reviews and are “problematic,” the report says.

Nearly half of Florida-based homeowner insurers are on a “watch list” developed by the Florida Office of Insurance Regulation, said Mark Friedlander, communications director for the industry-funded Insurance Information Institute (III).

“There is growing concern that several Florida residential insurers will be unable to complete their reinsurance programs for the 2023 hurricane season,” Friedlander said. “This could result in numerous financial rating downgrades and potential insolvencies.”

The ALIRT report observed that by offering insurers less coverage at higher rates, “it appears that reinsurers, worn down by years of substandard earnings, have also finally cried, ‘Uncle.’”

What’s to blame for rising costs?

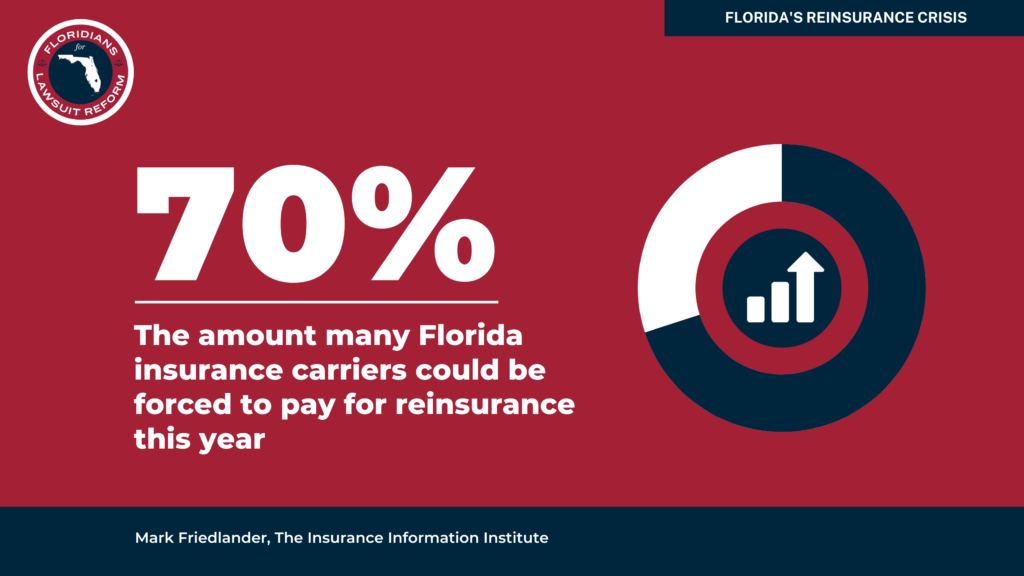

Of course, rising reinsurance costs will be passed directly to consumers. Friedlander says some companies could be forced to pay 70% more for their reinsurance this year.

ALIRT’s report stated that the looming reinsurance cost spikes are only partly attributable to litigation abuses that were addressed by the Legislature last year and earlier this spring, after being blamed for five years of rising premiums and collective industry losses.

While reducing lawsuits is “certainly a formidable step in the right direction, it occurs at a time when the Florida property insurance market faces another, perhaps equally existential challenge: obtaining the reinsurance protection so critical to the relatively small homeowners insurers that comprise the majority of this market,” it said.

A bigger reason for the upcoming price hikes is that reinsurers are waking up to Florida’s vulnerability to natural catastrophe after several years of costly hurricanes and other weather events “that many now attribute to climate change,” the report said.

Hurricane Ian, which caused an estimated $40 billion to $50 billion in damage after striking Southwest Florida last last September, is seen by the global reinsurance industry as the straw that broke the camel’s back after six years of global catastrophe losses, the report said.

The reinsurance industry, backed by global financiers looking for safe investments, has been reeling lately, averaging about $100 billion a year in from global catastrophes, according to financial analysis firm Moody’s.

Friedlander said III agrees that reinsurance rates for Florida-focused insurers are headed sharply higher but disagrees with ALIRT’s contention that litigation is a secondary factor this year. “Reinsurance renewals in other hurricane-prone states are expected to run much lower on average than Florida because those states don’t see the litigation abuse experienced here,” he said by email.

Despite restrictions enacted last year largely preventing third-party claims assignments and supplemental collection of legal fees in claims disputes, those enticements remain in place for policies active when the law took effect on Jan. 1. That means lawsuits over claims made before the reforms took effect can still be filed for years to come, delaying the reforms’ anticipated cost savings for insurers and any rate stabilization promised to homeowners.

Yet, Locke Burt, president and CEO of Security First Insurance Co., says the reforms have reduced the number of lawsuits filed against his company by 57% over the first four months of this year. He said, though, that the upcoming reinsurance cost increases will wipe out those savings.

For every $1 of insurance premiums that homeowners pay, about 20 cents goes to litigation claims, Burt said. “We think that’s going to be cut in half” in the near future, he said. Forty cents of the $1 goes to reinsurance and those costs are expected to increase for his company 30% to 40%, he said.

Reinsurance cost hikes passed to customers

According to ALIRT, Florida-focused companies paid reinsurers an average of 49 cents for every dollar of premium collected in 2022.

What does that mean for policyholders? Policyholders will generally see premium increases of roughly half of the percentage increases that insurers will see for reinsurance, says Paul Handerhan, president of Federal Association for Insurance Reform, a consumer watchdog organization based in Fort Lauderdale.

That means that if an insurer must pay 50% more for reinsurance this year, premium increases for policyholders will run about 25% on average, he said.

Handerhan expects all but a couple insurance companies will secure their needed reinsurance coverage for the upcoming hurricane season, but the increases will prove costly for policyholders.

He concurs that reinsurers are awakening to the increased costs of damaging storms. “There’s no doubt that climate change, including sea level rise, hurricanes and storms like the one that flooded much of Fort Lauderdale last month, are increasing in frequency and severity,” he said.

Were we paying too little?

ALIRT also suggests that Florida homeowners have been enjoying artificially low insurance rates — or in insurance-speak, “suppression of actuarily sound” rates — for the past three decades. The combination of suppressed rates and increasingly costly storms, the report said, “has proven a recipe for chronic (re)insurance losses.”

That’s because insurers rely on reinsurance coverage to pay claims after they spend a prescribed percentage of their surplus. Many companies, particularly startups, charged low premiums to compete for customers in the 10 hurricane-free years between 2006 and 2015, Handerhan said. As a result, many accumulated less surplus and are now weaker financially than if they had charged rates reflecting their actual cost of risk, Handerhan said.

If reinsurance costs rise year after year for a company that has seen its surplus erode for six or seven years, eventually that surplus is eroded to the point that the company can never catch up, he said.

Handerhan expects reinsurance rates to stabilize within two to three years, as last year’s legal reforms gradually reduce litigation costs, and as insurers are forced to cut costs by improving claims handling practices and shedding risky policies.

That means state-owned Citizens Property Insurance Corp. will still have to be the insurer of last resort for owners of older homes most vulnerable to damage from severe weather, he said. But eventually, premiums should stabilize for homeowners fortunate enough to be able to buy private-market insurance, he said.

ALIRT’s report warns that much depends on the weather.

About the only way out of trouble for Florida’s property insurance industry as it waits for the legal reforms to reduce losses is to “keep their fingers crossed on the catastrophe front,” the report said, adding that’s “never a great strategy.”

Ron Hurtibise covers business and consumer issues for the South Florida Sun Sentinel. He can be reached by phone at 954-356-4071, on Twitter @ronhurtibise or by email at rhurtibise@sunsentinel.com.,