The impacts of legal system abuse-driven social inflation has become a significant challenge for the U.S. casualty insurance industry, particularly driving up loss costs in lines such as products liability, general liability, commercial auto, and medical professional liability, according to AM Best.

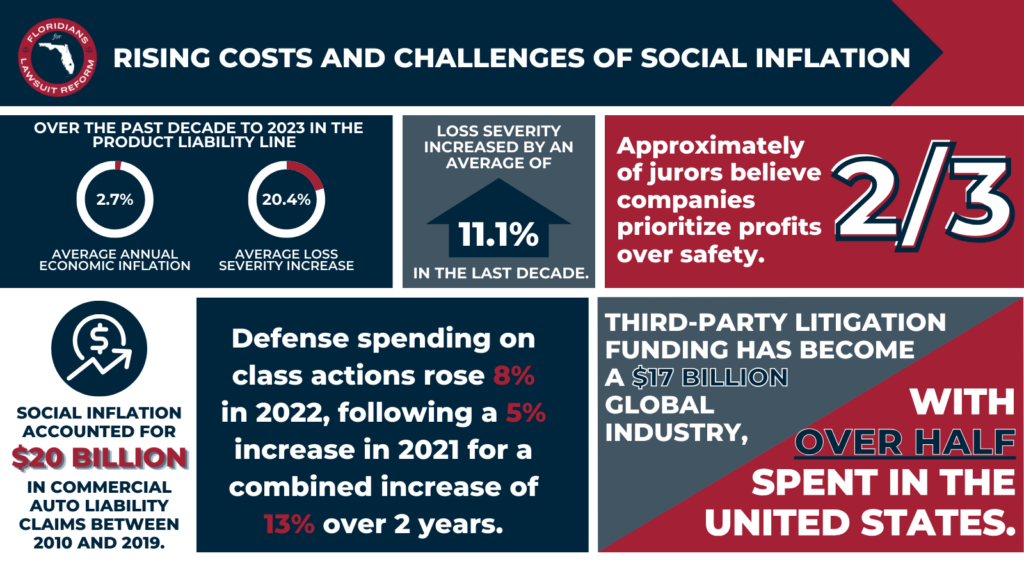

Loss severity for these lines has exceeded the rate of economic inflation, in most cases by double or more, with social inflation likely being a key factor, Best noted. For example, the average loss severity increase over the past decade to 2023 in the product liability line was 20.4%, compared with average annual economic inflation of 2.7%.

On the other liability–occurrence line, which captures excess liability and umbrella coverage, loss severity increased by an average of 11.1% in the last decade, the report found.

The growing involvement of attorneys in commercial lines is leading to an ongoing rise in claims costs, which negatively affects insurer loss ratios.

The social inflation phenomenon is characterized by dramatic increases in verdicts and settlements without the necessary legal or factual basis to support them, Best stated.

“The ‘social’ part of social inflation refers to shifting cultural attitudes about who is responsible for absorbing risk—the insurer or the plaintiff—and these dynamics continue to evolve, which makes social inflation tough to quantify and even more difficult for insurers to predict and mitigate,” said Justin Aimone, associate analyst, AM Best.

Public sentiment toward large corporations has been declining, with approximately two-thirds of jurors believing that companies prioritize profits over safety. Attorneys have capitalized on this sentiment, employing strategies like “reptile theory” and “juror anchoring” to obtain outsized awards.

A 2022 study by the Insurance Information Institute and the Casualty Actuarial Society found that “social inflation accounted for $20 billion in commercial auto liability claims between 2010 and 2019,” AM Best noted.

The rise in legal spending on class action lawsuits has also contributed to the issue. According to Carlton Fields’ 2023 survey, defense spending on class actions rose 8% in 2022, following a 5% increase in 2021. Companies cite larger claims and more class actions as the primary reasons for this increase.

Nuclear verdicts, characterized as those exceeding $10 million in punitive and compensatory awards, have been growing in both amount and frequency. A U.S. Chamber of Commerce review found that median nuclear verdicts were up 27.5% from 2010 to 2019, outpacing inflation. Product liability, auto accident, and medical liability cases accounted for roughly two-thirds of reported nuclear verdicts.

“When a nuclear verdict is awarded, it affects not just the one claim, but also all other open claims, as plaintiffs, guided by their attorneys, seek a similar verdict or settlement, rendering an insurer’s existing reserves inadequate,” said David Blades, associate director, industry research and analytics, AM Best. “The impact on adverse loss development then flows into pricing, as insurers adjust their view for the affected lines.”

Third-party litigation funding has become a $17 billion global industry, with over half that amount spent in the United States. Swiss Re estimates that investment in this market will reach $31 billion by 2028. When third-party funders back plaintiffs, the pressure to settle early or for reasonable amounts declines significantly, leading to prolonged legal battles and increased costs for insurers, according to the AM Best report.

Insurers face challenges in quantifying and predicting the impact of social inflation, as it affects the adequacy of reserves and shifts development patterns. When a nuclear verdict is awarded, it impacts all open claims, rendering existing reserves inadequate. This, in turn, flows into pricing as insurers adjust their view for the affected lines.

To navigate the complexities of social inflation, insurers must improve their understanding of portfolio risks and claims duration for better actuarial adjustments. Pursuing tort reform legislation on litigation funding disclosure and consumer protection may also help mitigate the impact. However, as social dynamics continue to evolve, addressing social inflation will remain an ongoing challenge for the insurance industry, according to AM Best.

To view the full report, visit AM Best website.