Farmers Insurance isn’t the only company to halt sales of new homeowners’ policies in Florida.

Fifteen other insurers have stopped writing new business in Florida over the past 18 months, according to the Insurance Information Institute (III), and three have voluntarily withdrawn from the market

“Companies have made decisions to stop writing new business for a variety of factors,” said Mark Friedlander, III’s director of corporate communications. “Many of them relate to what we call a man-made crisis of two issues, legal system abuse and claim fraud schemes. That’s what’s really driven Florida’s insurance crisis that we’re facing today.”

Farmers blamed historically high catastrophe costs and rising reconstruction costs on their decision to withdraw from Florida as hurricane season looms.

“We implemented a pause on writing new homeowners policies to more effectively manage our risk exposure,” Luis Sahagun, communications director for the insurer, previously told Insurance Journal.

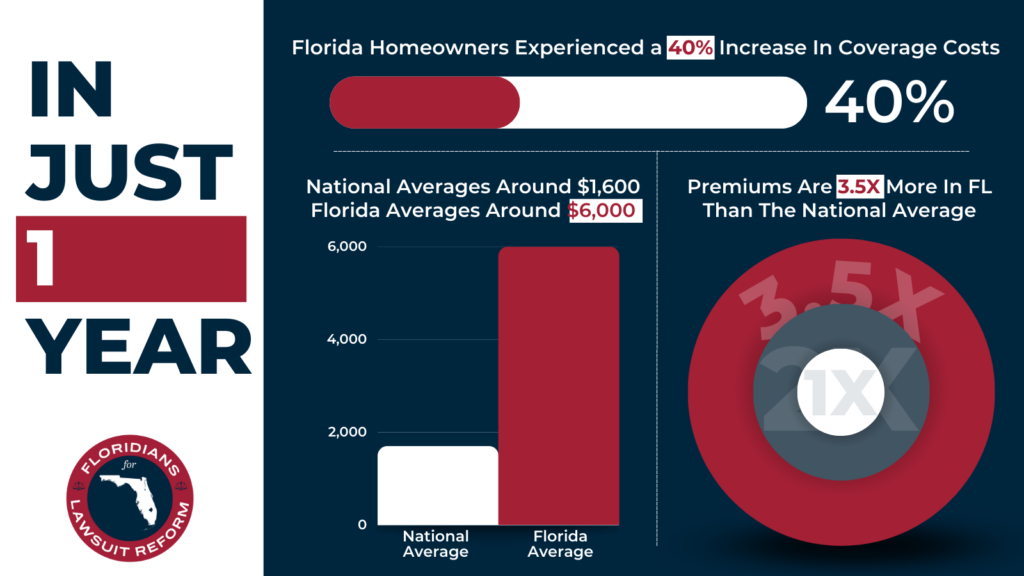

The Institute’s data shows that Floridians pay $6,000 a year on average for home insurance compared to the U.S. average of $1,700, which is 3.5 half times as much.

Year over year, Florida homeowners are paying 40% more on coverage in 2023 than a year ago.

“We have a very unstable property insurance market here in Florida,” Friedlander said. “There are some options with private insurers, but even the companies that are continuing to write business are limiting their risk. So, they’re not necessarily writing all types of risk in the state.”

As a result, Florida consumers are turning to Citizens Property Insurance Corporation, which is known as the state-operated insurer of last resort.

With a market share that’s 50% higher than last year, Citizens Property Insurance Corporation has grown to more than 1.3 million customers, according to III analysis, and is the largest home insurer statewide. The state entity is also averaging more than 30,000 new customers a month.

“That’s a really bad situation because backstop insurers are not supposed to be your insurer of choice,” Friedlander told the Florida Record. “It’s only supposed to be a backstop for consumers who can’t find coverage. It was never intended to be bigger than private companies. But, because of the volatile situation we’ve been facing for many years, that’s what we see today.”

The government-owned insurer was created in 2002 and 21 years later is requesting a 14.2 percent rate increase, according to media reports.

Last year, Citizens sought an 11% increase and were only allowed a 6.4% hike.

“By regulation, Citizens is not allowed to charge enough rate for the risk they are writing so that leads to a potential major shortfall if they have to pay out a large storm claim,” Friedlander added. “When you see a state plan growing so large and extending its risk so heavily to a point where possibly surcharges are gonna be enacted against all sorts of consumers you have, you have a real problem on your hands. It’s a very bad model for success and it just shows how bad the private market has been.”